Want to know more?

Avant Research offers complimentary consultations to determine how our project management and technical consulting services can help you.

Call (03) 8567 7500Business hours 9am-5pm, Monday-Friday

(Australian Eastern Standard Time)

OR

Send us an email

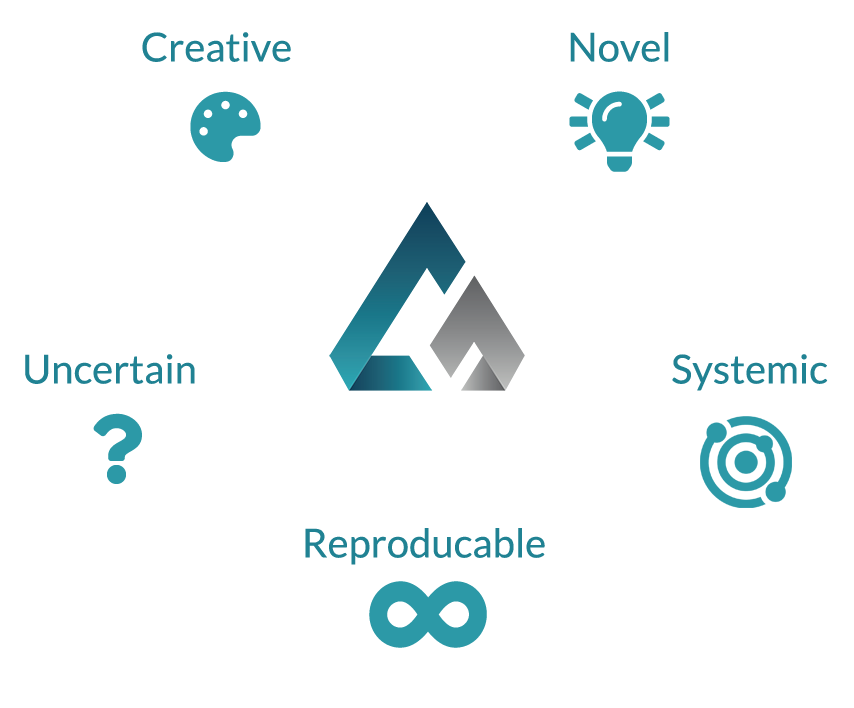

R&D Identification

For an activity to be considered research and development (R&D), and therefore eligible for the R&D Tax Incentive, it must meet the following criteria:

Novel

An R&D project aims to create new knowledge. For university research projects, entirely new knowledge advances are expected to be pursued.

For businesses, whether a project is considered novel will be based on the current knowledge within an industry.

For findings to be considered novel, they must:

- Be new findings to the business

- Not already exist in the industry

R&D activities that are done to copy, imitate or reverse engineer as a method of gaining knowledge are not considered novel and are therefore excluded from the R&D Tax Incentive.

Activities that are considered R&D:

- An experimental development project aimed at creating knowledge in support of the development of new concepts and ideas related to the design of new products/processes

- Integration of a very complex system, with additional material emerging from practical experience in ordinary maintenance and properly codified, as long as this is done as part of an R&D project

- Systemic testing to provide documentation of the potential use of a chemical reaction that has already been adopted in production processes i.e. an existing technology, in order to achieve a new molecule, which has been considered an improbable outcome by the scientific literature

Example: In the medicine field, a routine autopsy to determine the causes of death is medical care practice and is therefore not R&D. In contrast, a special investigation of a particular mortality to establish the side effects of certain cancer treatments is R&D, as it is novel and there is uncertainty about the study’s final results. There is also transferability of the results for broader use.

Creative

R&D is about aiming to discover new and original concepts or ideas that improve on existing knowledge. Products and processes that are considered routine are excluded from R&D.

Creativity requires human input, therefore any R&D project requires the contribution of a researcher.

Although routine activity is excluded from R&D, new methods to perform common tasks may be included. For example, data processing is typically not an R&D activity. However if it is part of a new project that aims to develop new methods for data processing, it may be considered an R&D activity.

Arts activities need to take care when assessing R&D activity. Although the arts are a creative field, the activity must also satisfy the other criteria – i.e. Novel, Uncertain, Systemic and Reproducible, to be considered.

Uncertain

For an activity to be R&D, the outcome and cost must be uncertain i.e. cannot be precisely determined relative to project’s goals.

An independent expert in the field would not be able to determine the results from the activity before it is conducted for example.

There should be uncertainty around the costs and time needed to achieve the results, as well as whether the objectives can be achieved at all for an activity to be eligible.

This criterion is key when distinguishing between R&D prototyping e.g. models used to test technical concepts and technologies with a high risk of failure and non-R&D prototyping e.g. pre-production units used to obtain technical or legal certifications.

Systemic

An R&D activity must be systemic, which means it is conducted in a planned way, with records kept of the process followed and the outcome.

To verify this, sufficient contemporaneous records must be kept throughout the entire R&D activity.

Reproducible

An R&D project should result in the potential transfer of new knowledge, therefore other researchers should be able to reproduce the results as part of their own R&D activities.

This includes negative R&D results, i.e. an initial hypothesis that fails to be confirmed or a product cannot be developed as originally intended.

In a business environment, the results be protected by intellectual property protection, however it is expected that the process and results will be recorded for use by other researchers in business.